What are the Types of Business Entities?

Updated:

Business entities are essential for starting, managing, and growing your business.

Looking for information on business entities in the United States? See our state-by-state guide to business entities in the United States. Want to see business entities for other countries? Check out our international business entities guide where you can search by country or global region.

Types of Business Entities

“Business entity” is a generic term with no legal significance per se. A business entity simply refers to the form of incorporation for a business. When a business incorporates, the law recognizes the business as a distinct entity which can enter contracts and acquire property among other rights and privileges.

There are, of course, some exceptions like sole proprietorships and general partnerships, which do not require incorporation. They also do not have the same right and privileges as incorporated legal entities.

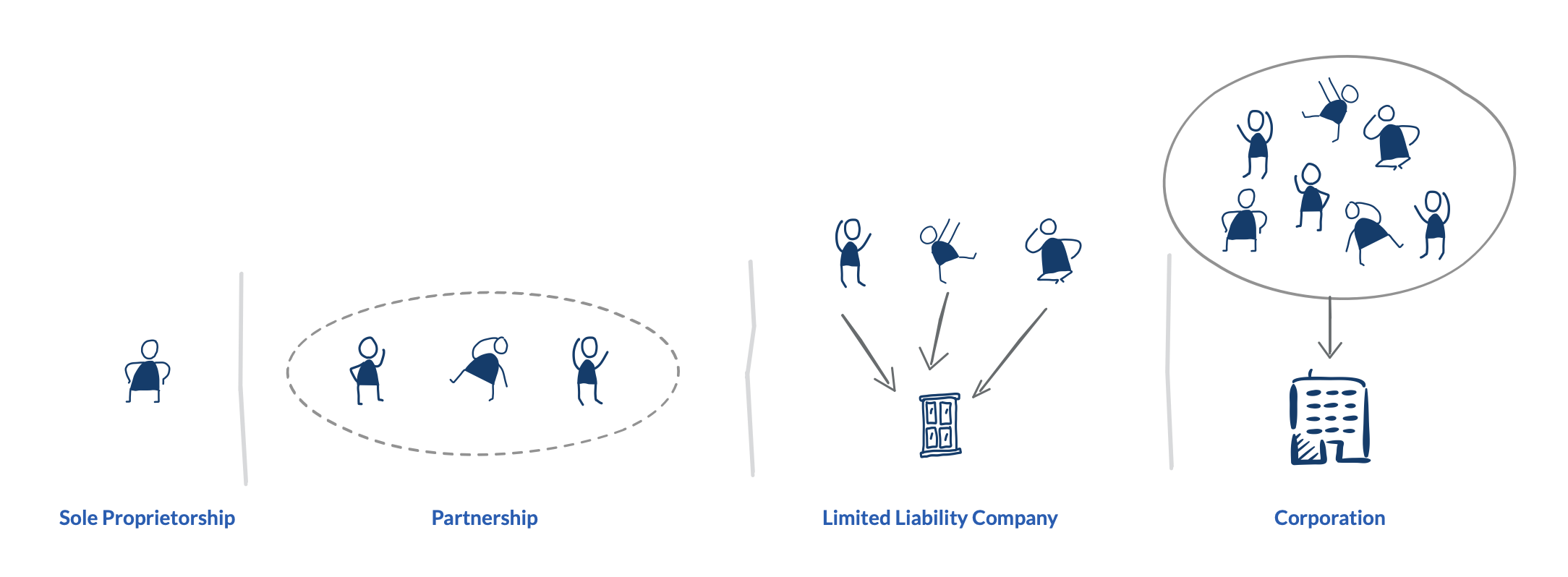

There are four broad groups of business entities: limited liability companies, corporations, partnerships, and sole proprietorships. There are important flavors of each class of business entity.

LLC

A limited liability company (LLC) is a unique form of business entity. LLC owners are called members. The people who run an LLC are called managers. However, the organizational documents can change this terminology. There are, generally, no restrictions on the number or type of owners of an LLC.

Limited liability companies (LLCs) have grown in popularity for new, privately held businesses. They have eclipsed S Corporations as the preferred business entity for start ups and small businesses based on historical US tax data. That does not mean an LLC is the right choice for every business by any means.

There are two main reasons people choose LLCs. First, they are flexible in their management structure. It is easy to create LLCs which have the formality of a corporation with officers and directors, or informal management like a partnership.

Second, LLCs typically provide pass through tax treatment. Pass through tax status, like partnerships, means that the business does not pay income taxes on its income. Instead, income is allocated to the members who then pay taxes on their share.

There are three types of limited liability companies: member-managed LLCs, manager-managed LLCs, and professional LLCs. Not all jurisdictions have all types. The bundle of rights and obligations might also differ across jurisdictions.

Member-managed

A member-managed LLC resembles a traditional general partnership. Each member (owner) can enter contracts for the entire LLC, binding the entity. Member-managed LLCs are common because they are simple and the founding members are the same people operating the business.

Manager-managed

Manager-managed LLCs separate the ownership and management functions. In a manager-managed LLC, the member choose a manager (or managers) to run the business. In that case, only the manager can enter legal contracts for the LLC. Manager-managed LLCs more closely resemble corporations in this way. In fact, manager-managed LLCs often adopt the terminology of corporations in the by-laws and operating agreements, referring to a board of directors and corporate officers like a president and CEO.

Professional Limited Liability Company

States regulate the types of business entities that licensed professionals can use to form a business. Licensed professional include, lawyers, accountants, architects, doctors, engineers, and the like. Some states have created a special LLC, called the Professional Limited Liability Company (PLLC) for this purpose. Other states do not authorize PLLCs, but do have alternatives like Registered Limited Liability Partnerships or Professional Corporations.

It is especially important to make sure which type of professional entities are available in a particular state, which professions may use the entity, and what the rights and obligations are.

Corporation

Corporations are one of the oldest forms of business entity. Corporations are one of the oldest forms of business entity. Corporations are owned by shareholders, who can be individuals or other entities. Shareholders are issued stock (or shares) in exchange for investment of money or something of value, like intellectual property or an employment agreement.

Shareholders vote for a board of directors, who in turn select officers to manage the company. Officers run the day-to-day business, while the directors oversee the managers. The board of directors is also responsible for certain types of decisions such as mergers and acquisitions, sales of major assets, and bankruptcy.

Corporations are the preferred legal entity for businesses that are or plan to be publicly traded. Accessing public markets for investment capital is not the only reason to choose a corporation.

There are primarily three types of corporations that businesses form based on sections of the Internal Revenue Code: Subchapter C Corporations (C Corp), Subchapter S Corporations (S Corp), and Non-Profit or Not-for-Profit Corporations:

C Corporation

A C Corporation is the most common business entity for large companies and those which are publicly traded. While there are many reasons businesses choose the C Corporation form of legal entity, the primary driver is corporate finance law.

As a general rule, corporations must pay entity level taxes. This general rule is heavily modified by the subchapters of the tax code that apply. S Corporations, for example, may provide pass through tax benefits.

Corporations are subject to double taxation. Double taxation is the idea that the entity itself pays taxes on its income, and then the owners pay income taxes on the dividends which they receive from the corporation.

The law about raising capital and managing for-profit companies is well established and generally reliable. Subchapter C does impose double taxation, but the ownership and management flexibility more than compensates for the tax burden.

New businesses and start-ups may choose to create a C Corporation when they know they are on a path to multiple rounds of fundraising, which will culminate in a sale of the entire business or taking it public.

S Corporation

S Corporations are, roughly speaking, an earlier form of a limited liability company in that they combine the tax benefits of a partnership with the liability protections of a corporation.

There are ownership restrictions for S Corps that do not apply to LLCs.

Non-Profit Corporation

There are many types of charities or non-profit organizations based on the Internal Revenue Code. The most prominent type is the 501(c)(3) public charity.

Partnership

Partnerships can be informal business entities, which means there are no filing requirements and few, if any, maintenance requirements. Partnerships are not generally recognized as business entities for tax purposes, which means profits and losses are allocated to the partners individually as a pass-through.

There are number of risks to a partnership that warrant careful attention. The most important risk is that any partner in the partnership can bind all the other partners so that each partner is individually liable for each obligation of the entire partnership. There are certainly ways around this problem and a number of statutory alternatives have emerged, but founders should be thoughtful about partnership formation.

There are several types of partnership under common law and state statutes: general partnerships, limited partnerships, limited liability partnerships, and limited liability limited partnerships.

Many states have adopted variations of the Uniform Partnership Act (1997) and the Uniform Limited Partnership Act (2001).

General Partnership

A general partnership is disregarded for tax purposes. However, partners are strictly liable for the debts of the partnership. Debts includes financial indebtedness from any source as well as contractual obligations. A general partnership must have at least two general partners (GPs).

Limited Partnership

Limited partnerships have a general partner and at least one limited partner (LP). A limited partner has no management authority and cannot generally bind the partnership. The GP retains all the management authority. Limited partners are usually financial backers who participate in the proceeds.

The general partner has liability for conduct of the partnership, whereas each limited partner’s liability is capped at the investment in the partnership.

Limited partnerships are popular for project based businesses such as real estate development and investing. The GP is typically a corporation which seeks out LPs to raise financing for a project.

Limited Liability Partnership

Unlike limited partnerships, limited liability partnerships do not have a separategeneral partner. Each partner has limited liability protection and there is no general partner with unlimited liability. The scope of limited liability varies widely from state to state.

In this way, the LLP resembles an LLC, because the partners have limited liability and benefit from pass through tax treatment.

LLPs are often used in professional industries where malpractice by one partner might affect the entire partnership.

Limited Liability Limited Partnership

The limited liability limited partnership (LLLP) is not widely used. LLLPs are also not available in every state. An LLLP is a sophisticated business entity designed primarily for investment purposes. It shares many of the characteristics of limited-partnerships, except that the general partner gets additional limited liability protections.

Sole Proprietorship

As the name implies, a sole proprietorship is a one person business entity. A sole proprietorship is not incorporated, avoids double taxation, and does not provide any liability protection. The assets of the owner are fully exposed.

For example, if a sole proprietor opens a coffee shop and gets sued for an accident at the shop, then the owner’s house, car, and bank accounts are available for the successful plaintiff.

Notwithstanding this risk, sole proprietorships are quite common, because individuals want to avoid the cost and hassle of setting up and managing a separate legal entity.

Key Concepts

Business entity and legal entity are used interchangeably. A legal entity is distinct from a natural person. A legal entity is recognized by a government. It can enter contracts in its own name. A legal entity can sue and be sued. It can maintain bank accounts and buy insurance. In short, a legal entity can usually conduct all the commercial activity that an individual can.

To understand business entities better it is helpful to know about some core concepts: person, ownership, management, tax status, compliance, and jurisdiction.

Person

There are two types of “person”: natural and legal. A natural person is what you commonly think of when someone says “person.” It is a human being. A legal person is an artificial entity recognized by the law as a person.

Natural Person

Natural persons might have restraints on their legal capacity. For example, they only acquire their full citizenship rights at the age of majority. People declared legally incompetent also cannot enter contracts.

Natural persons can own property individually or with others. They can enter contracts, pay taxes, and engage in political activity.

Legal Person

When a government recognizes a legal entity, the government confers certain rights and responsibilities on that entity. Legal entities might have restraints on their legal rights.

In many countries, legal entities can own property, enter contracts, and pay taxes. Legal entities may or may not have the right to engage in political activity in their own name.

Notice that most of the business related rights are common to natural and legal persons. This is a foundational concept when forming a business. You are incorporating a legal entity which can do most of the things you can do.

Ownership

Legal entities do not appear out of thin air. Legal entities have owners. Individuals and other entities (sometimes) can own a legal entity.

There are two aspects to ownership of legal entities. An owner can have an economic interest and a management interest in a company.

Economic owners

An economic interest means that an owner has the right to receive profits of the legal entity. This does not mean that the entity has obligation to distribute profits to the owners in the form of dividends or distributions.

Rather, an economic interest means that the owner has a claim on the financial value of the enterprise. If the business is sold, for example, owners receive a pro rata share of the proceeds after creditors are paid. A pro rata share is a proportional share. If someone owns 5% of a legal entity, then when that entity is sold, that owner will receive 5% of the sales price.

The simplest example of a purely economic owner is someone who holds a share of stock in a publicly traded company. If you own a single share of Google (now trading as Alphabet, Inc.), you have the right to receive approximately 1/349,480,000th of the sales price if it were ever acquired. Congratulations!

However, you have no right to appoint people to the Board of Directors of Alphabet. Although you can probably vote your share for a slate of directors.

Management owners

An owner who can make decisions on behalf of the legal entity has management rights. A management owner might exert that authority somewhat indirectly by participating on the Board of Directors, or by working as an officer in the company, such as the President, Chief Technology Officer, Managing Director, or similar title.

For most start ups, the founders have both economic and management interests. It is easy to muddle these roles. Keeping them distinct, however, can improve your financial success.

Management

Management refers to the people appointed by the owners to oversee the day-to-day operations of the business entity. The terminology for management can vary between corporations and other forms, like LLCs. For clarity and simplicity, we will use the corporate terms: directors and officers.

Directors

Owners appoint directors to represent them on the Board of Directors. In small and medium businesses, owners will usually just appoint themselves.

At a minimum, directors will conduct annual meetings and appoint the officers. The organizational documents may also reserve certain decisions about the business to the directors instead of the officers. Common examples includes mergers and acquisitions, sale of major assets, and bankruptcy.

Officers

In a corporation, managers are typically called officers. LLCs call them managers, but often change the title to officer in the organizational documents. Non-profit companies might create an “executive director” role.

The management roles created by the organizational documents (by-laws) are those positions that have authority to direct the daily business of the company and to enter contracts.

Tax Status

Tax law applied to legal entities is complex. The choice of legal entity can have lasting consequences for taxes owed and paid by both the business entity itself and the owners.

While there are state and local tax implications, most discussion of entity taxation focuses on federal taxes. In broad strokes, entities are either disregarded for tax purposes or they pay entity level taxes.

Pass Through Taxes

When an entity is disregarded for tax purposes, we say that it benefits from pass through tax status. Pass through entities do not pay taxes on their business income. Instead, the owners pay income taxes on their share of the income from the business. The income is deemed to “pass through” to the owners and so does the tax obligation.

Pass through tax status avoids the problem of double taxation.

Entity Level Taxes

Corporations in the United States are subject to double taxation. What does double taxation mean? Double taxation means that the entity pays taxes and then the owner pays taxes on dividends or distributions.

Imagine a company has gross sales of $1,000,000. After its cost of goods and operating expenses it has a profit of $100,000, or a 10% net margin. It decides to distribute 10% of the profits (before taxes), or $10,000 to the shareholders.

The corporation, however, must pay taxes on its profits before distribution to shareholders. So our company must pay $35,000 dollars out of the $100,000 in profit as corporate taxes, using an effective tax rate of 35%.

So now, the company distributes 10% of $65,000 ($100,000 profit - $35,000 taxes) to shareholders, or $6,500 instead of $10,000, as a dividend.

What about that $6,500? Double taxation means that the shareholders who receive the distribution, must pay individual income taxes on the dividend. Using an example income tax rate of 33%, the shareholder must pay $2,145 in taxes, leaving $4,355. So the shareholder starts with a $10,000 potential distribution and ended with a $4,355 distribution.

But there are lots of good reasons for the corporate form. For example, maybe the growth strategy means that the company will retain profits and not distribute them. In that case double taxation is not a problem. A limited liability company might be a disadvantageous form in that case.

Compliance Obligations

When you incorporate, you must maintain the legal entity to preserve the benefits. Each jurisdiction is different, but they all share some periodic filing and the payment of a fee of some kind. Miss the filing or fail to make the payment, you risk the legal shield of the entity, not just for yourself, but for every owner and officer in your organization.

To avoid that risk you can pay additional fees to a registered agent or use legal entity management software.

Jurisdiction

Jurisdiction refers to the part or level of the government which has authority over a business entity. The federal government has jurisdiction over federal taxes, but the state where the entity is incorporated has jurisdiction over the corporate law of the business.

The most important jurisdiction concepts for business entities are the place of incorporation and the principal place of business.

Place of Incorporation

Where you incorporate and where you do business are two different questions. We will start with the Place of Incorporation. Most businesses will incorporate in the state where they will do business and where the owners live, but that does not have to be the case.

The United States has no national registration system; businesses are incorporated in one of the 50 states. The state where a business incorporates is called the place of incorporation. As a general rule, business can incorporate in any state. Many business incorporate in Delaware because of its well established corporate law.

Principal Place of Business

The principal place of business is the jurisdiction where the business has its headquarters. A business can incorporate in Delaware and have its principal place of business in Texas, even the owners live in California.

Implications of Jurisdiction

There are several implications that flow from the jurisdictions where a business chooses to incorporate and conduct its business.

Choice of law for legal entities

The place of incorporation will determine which types of legal entities are available. Not all entities are available in all jurisdictions.

Cost

There are two costs to consider when choosing a jurisdiction. First, what is the cost of the filing fees, there might be many depending on the number of steps. You should also understand the costs to renew and maintain that registration in your jurisdiction.

Second, some jurisdictions have minimum paid-in capital requirements. In other words, you must raise or contribute a minimum amount of money just to register the company. This requirement can also depend on the type of legal entity in that jurisdiction.

Time and procedures

Registering a new legal entity can be quick and easy or long and arduous.

Taxes

Your choice of jurisdiction will also affect the taxes your legal entity must pay.

Investor signaling

If raising money from professional investors, like angel investors or venture capitalists, is an important part of your plan, then the choice of jurisdiction can signal investors about the attractiveness of your legal entity.

Obviously, the financial statements and business plan are more important, but if you incorporate in a jurisdiction that is hostile to minority shareholders or is unfamiliar to investors, then your choice will hinder your ability to raise money.

Qualification to incorporate

Make sure to understand who can incorporate a business in your jurisdiction of choice. Jurisdictions impose residency, citizenship, age, and type of person restrictions. Your type of legal entity might also limit the number and type of investors or owners.

DBA

You can also create fictitious or trade names for the business. These are often called DBAs (Doing Business As). Imagine you incorporate the Wallin Smith Technology Products and Services Company, LLC in Delaware. Wallin Smith Technology Products and Services Company, LLC is a marketing mouthful. So you decide to do business as: “Wallin Tech.” Wallin Tech is the legal entity’s trade name.

You register that DBA in the jurisdiction where you are incorporated and where you do business to protect it and to comply with local law about disclosing trade names.

Foreign company registration

Most jurisdictions require companies that are not incorporated in the jurisdiction to register or get permission before doing business in the jurisdiction.

This is called a foreign company registration, but “foreign” is not just for international businesses. If you incorporate in Delaware, for example, and do business in California, you will probably need to register as a “foreign” corporation in California.

Sometimes you might to incorporate a second legal entity in the other jurisdiction; otherwise you will simply register as a foreign corporation.

Between countries, however, the foreign registrations can be more difficult. Some countries impose significant restrictions on foreign companies doing business locally. You will likely need to designate a local agent for service of process and to meet residency and citizenship requirements.

Choosing a Business Entity

Once you know where you want to register your business, you must choose your type of legal entity. While legal entities are not quite like ordering food off a menu, after you choose the restaurant, you do have options.

Choices: jurisdiction + entity type

Best choice of available options under prevailing circumstances

There are many considerations for choosing a legal entity type. This is not an exhaustive list.

Criteria

When choosing a legal entity, ask

- What is the cost?

- How complex is the process?

- Are their constraints on your management plans? and

- Will it support your financial and tax objectives?

Cost of Incorporation

Registering a legal entity costs money: sometimes a little; sometimes a lot. Costs include the filing fee, renewal fees, professional fees, and franchise taxes. These are direct costs.

Filing fees

Every jurisdiction imposes a filing fee. Fees change frequently. There are often fees for particular kinds of filings. Fees might also vary by type of entity. Review the fees for your jurisdiction and entity type carefully.

Here, for example, are the fees for the Delaware as of August, 2018.

Renewal fees

Registering a company is not a one time event. You must renew the registration to keep it current. Not all registration renewals are annual. Some jurisdictions do not require renewal for several years. Simply do the math to annualize registration fees to compare them from jurisdiction to jurisdiction, or entity type to entity type.

Professional fees

There are three types of professionals you may need to pay: lawyer, accountant, and registered agent.

Legal fees for incorporation can be modest or breathtaking. Business lawyers should be able to tell you about the costs for incorporation in your jurisdiction before starting any work. Legal fees can rise quickly to cover complexities beyond the registration.

Fees for accountants follow a similar pattern. Providing initial tax advice and setting up your accounting might be one cost, but getting help with complex asset transfers, foreign accounts, and the like, can quickly raise the costs.

Good legal and accounting advice early in the process is money well spent.

Registered agents, sometimes called “local agents”, are people or companies that are empowered to accept legal notices on behalf of the business. The registered agent address is published to the world. While you can often be your own registered agent in your own jurisdiction, you might choose to use a registered agent so that any legal notices does not get mishandled.

Franchise tax

Not all jurisdictions impose a franchise tax, but many do. A franchise tax is basically a tax on the business’ balance sheet. It might be tied to assets or to net worth. The idea is that your registration and renewal fees are determined in part by the assets of the business.

If the entity operates an “asset light” business, like consulting, then the franchise tax might be low for a long time. However, an asset intensive business with equipment, real estate, or large cash balances, then the franchise tax will be a material consideration.

This is an area where good accounting advice about recording the value of your assets is helpful.

Ease of Incorporation

It is not difficult or time consuming to incorporate many entities in jurisdictions that encourage incorporation. The time and effort, however, can vary. Your local lawyer will have the most accurate estimate, but there several factors to consider: total time, number of steps, incorporator requirements, minimum capital required, and the number and type of investors.

You can use the World Bank data to get benchmarks to help you estimate. While the World Bank data includes some subnational jurisdictions, like states in India, it does not include any data for individual states in the United States. You cannot compare Delaware to California and New York, for example.

Management Requirements

Some jurisdictions and entity types require named officers or certain board structures. You can often satisfy those compliance requirements without interfering with your management plan for operating the business.

For example, if you must name a President and Secretary as authorized signers and you have a co-founder, then one of you can serve one role while the other serves the other function. This choice does not necessarily have any effect on the management team you put in place.

Some jurisdictions also impose a dual board structure where one board is charged with governance matters and the other is the operational management board. Before chasing a dual board structure, make sure that it is required in your jurisdiction for your size and type of business.

Tax and Financial Objectives

One of the most important factors when choosing a legal entity is the tax treatment of that entity’s income. The place to start is the financial objective for the business: current income or growth. Of course, everyone wants both income and growth, but it is a question of priority and scale.

Consider two business: Great Service Group and Fast Product Company. Great Service is an information technology service and consulting business. The owners want to take as much money out of the business for their personal income as possible.

Fast Product makes a mobile app with global market potential. The owners of Fast Product want to reach the largest market possible as quickly as possible. They only need a minimal income.

Both companies want to incorporate in Delaware, because of the well establish corporate law and ease of incorporation. However, which type of legal entity should each choose?

From a tax perspective, a corporation is a bad choice for Great Service, because they will have to pay double taxation. Great Service will have to pay income tax on its sales directly. When Great Service pays the owners through salaries and/or dividend distributions, the owners will pay personal income tax.

If Great Service incorporates as a Limited Liability Company (LLC), then the Internal Revenue Service will treat Great Service as a disregarded entity for tax purposes and only tax the distributions to the owners.

A corporation is probably the right choice for Fast Product, because the owners will not take much as a distribution. Fast Product will show little profit subject to corporate tax rates because they are spending to grow the business, which means expenses are high. The company is paying small salaries to the owners so they do not pay much personal income tax.

Income versus growth is just one consideration informing your selection of legal entity. The choice is rarely this simple. Being clear about your financial objectives can help clarify your entity selection.

Tax Considerations

The choice of where to incorporate and the type of entity to create have important implications for your taxes. Jurisdictions impose a variety of types of taxes.

Types of Taxes

Jurisdiction may impose one or more of the following taxes: personal income, business income, franchise, property, consumption, and capital gains.

Incorporating a business will probably affect your personal income. It might go up or go down, depending on the choices you make and your objectives. The critical question is how will your tax jurisdiction treat your income from the business.

What is the applicable tax rate for business income in your jurisdiction? The choice of legal entity is probably less important than the character of the income. Current and qualified tax accounting advice in your jurisdiction is important.

The place of incorporation may also impose a tax on the business’ assets or net worth in the form of a franchise tax. A franchise tax is typically imposed at the time of registration and renewal by the jurisdiction where the business is registered.

Jurisdiction also strongly influences property taxes. Any layer of government might impose taxes on property the business owns or acquires. If the business is asset intensive, then property taxes can influence where you decide to incorporate and operate.

Consumption taxes come in two flavors: sales and use taxes (“Sales tax”) or value-added taxes (“VAT”). End consumers pay sales tax that is collected by a retailer who sends it to the taxing authority. VAT, on the other hand, is paid at each step of the supply chain. Sales and VAT regimes impose different administrative burdens on your business. Sales tax is the consumption tax used by states in the US.

Finally, capital gains taxes warrant consideration. A business might generate capital gains, which are profits on the sales of things not in the ordinary course of business, such as selling a building. But the most significant capital gains event is the sale of the business after it is wildly successful. How will the jurisdiction tax that event? As a practical matter, there might not be much choice about where to live and run the business.

International Taxes

A quick word about a long, complex subject: international income taxes. If a business sells products and services across national boundaries, tax advice from a tax professional is critical.

Countries tend to take either a territorial or residence approach to taxation of income earned outside the business’ home countries.

The territorial system only taxes income earned within the country. Whereas, the residence system taxes income earned globally for every company residing in the territory.

Hong Kong, for example, generally uses a territorial tax system. A Hong Kong company will pay taxes earned from sales in Hong Kong, but not on income earned in Australia and Malaysia. If, however, the Hong Kong company registers in Australia and/or Malaysia, then it will be subject to those countries tax regimes.

The United States is one of the most prominent examples of the residence system. US companies pay taxes on income generated in the US. US companies also pay taxes on global income, once that income is repatriated to the United States. In this example, income from Canada and Mexico are repatriated and taxed.

So knowing where your customers are and how you will reach them can affect your income tax bill and therefore the financial success of your business, and ultimately where you decide to incorporate your business.

Maintain Business Entities

Forming a business is a one time event that creates a long string of maintenance tasks for as long as the entity is a going concern. Limiting liability and asset protection are primary objectives for forming a business entity. Maintenance preserves those benefits. Without careful maintenance of the legal entity, it might not provide protection when it is needed most.

Over time things change for every business entity. Those changes are easily filed and forgotten. To keep in compliance and reduce risk from legal entity management, there are five buckets of information to track: entity summary data, company documents, filing requirements, officers and directors, and owners.

Entity Summary

As a general rule, it is useful to keep basic data about a business entity in one place. Basic information includes:

- Legal name,

- Legal address,

- Jurisdiction (place of incorporation),

- Form of organization,

- Registered agent name and contact information, and

- Incorporation date.

This information changes infrequently.

Documents

Company records and documents are critical for compliance and preserving the corporate veil. The corporate veil is the legal term for the limited liability provided by the form of legal entity.

There are a variety of ways to organize corporate documents and records. A useful scheme would include: organizational documents, filings and registrations, agreements, meeting minutes, risk management, and other.

Organizational Documents

Organizational documents include all the filings and paperwork that created the legal entity in the first place. The title of those documents varies by state and by legal entity type. Common organizational documents include: Articles of Incorporation, By-Laws, Operating Agreements, and Stock Certificates (or other evidence of equity ownership).

Filings and Registrations

Filings and registrations refer to documents created annually (or as necessary). Most states, for example, require that businesses file an Annual Statement or Annual Report. For businesses that operate in more than one state, the business likely needs to file a “Foreign Authorization” to do business outside the jurisdiction of incorporation.

Agreements

While legal entity management is not contract management, it is useful to keep important corporate agreements with the business entity documents.

Most entities have a some form of Ownership Agreement, such as a Shareholder Agreement for corporations, Membership Agreement for LLCs, and a Partnership Agreement for partnerships. Organizations might also have a Management Agreement.

If the owners are contributing some form of property, then there will be documents related to that property. For example, a founder who contributes real estate in exchange for equity will execute a transfer of that real estate.

A legal entity might also license intellectual property from one of the owners. That license agreement, whether it is a patent, copyright, or trademark, should be stored as a corporate document with the entity record.

As a bonus, agreements which have expiration dates or auto-renewal could trigger an automatic alert that the expiration is coming.

Meeting Minutes

The meeting minutes created during shareholder meetings or board of directors should also be part of the legal entity record.

Risk Management

Insurance policies that pertain the business could also be stored with the corporate records. In particular, Directors and Officers policies (D&O insurance) and Errors and Omissions policies (E&O insurance) might be filed in the risk management folder.

Other

While an Other bucket is not per se useful, there are likely additional collections of documents which you might want to add.

Requirements

Requirements are business entity obligations. For example, a business entity must file an Annual Statement each year. The business might operate in a regulated industry where it must file for a permit or license every year.

Other examples of requirements include DBA filings (Doing Business As, or trade name filings). States require companies conducting business in the state but not incorporated there to file for a Foreign Authorization.

People

There are several types of people associated with a business entity. Two groups of people are especially important: officers and directors. These terms usually apply to corporations, but the concept is important for most business entities. There are representatives of the owners (directors) and those who manage the business (officers).

Directors might have a term of service. They also might serve on committees for larger boards. Officers or managers have job titles and terms of service as well.

Owners and Investors

Last, but not least by any stretch, are owners and investors. Keeping track of the ownership interests in any business entity is critical. There are four elements to be mindful of when it comes to tracking owners and investors: parents, subsidiaries, unrelated owners, and company organization charts.

Parents

A parent is an immediate, direct owner of some or all the equity of a particular entity. If three founders form an LLC called NewCo LLC and they each have one-third of the membership interests, then all three are parents of NewCo LLC.

Subsidiaries

A subsidiary is a business entity owned wholly or in part by another business entity. For example, if NewCo LLC owns EastShop, Inc. and WestShop, Inc., then EastShop and WestShop are subsidiaries of NewCo LLC.

We can also say that NewCo LLC is the parent of EastShop and WestShop. Notice that we do not say the founders are parents of EastShop and WestShop, because they are two layers up in the ownership structure.

Related and Unrelated Owners

As a business entity accumulates parents and subsidiaries, we need a corporate registry to list all the legal entities under management, because each entity has its own documents, owners, compliance requirements and so forth.

Imagine that EastShop and WestShop jointly own SouthShop, LLC. The corporate registry would list four entities: NewCo, EastShop, WestShop, and now SouthShop.

However, if the founders decide to let an outside investor, named OVest Group, LLP, invest in SouthShop, OVest would not appear in the corporate registry because the founders and NewCo management have no responsibility for OVest as a legal entity. They certainly want OVest to appear as an owner, but OVest is an unrelated owner.

Company Org Chart

A business entity organizational chart is a visual representation of the ownership structure.

Some org charts are simple, but many are not. Org charts need to handle generation skipping, where an owner owns a company both directly and indirectly. It also needs to show related and unrelated entities.

As ownership details change the org chart needs to reflect those changes automatically, which is one of the reasons hand drawn org charts are dangerous. They capture a point in time at best.

Conclusion

Business entities are tools to help build a business. Some tools are better for certain jobs. Knowing which business entity to use and how to structure one requires the advice of a licensed lawyer retained for the purpose.

After the legal entity formed legal entity management software is a critical tool for maintaining the structure you built.